Many trucking businesses face this exact wall: they're operating legally, hauling legitimate freight, and still can't get quoted. New ventures hit the two-year rule. Hazmat haulers get flagged for cargo type. Owner-operators with a single at-fault accident find their options suddenly narrow. NHTSA reported 5,472 fatalities in large-truck crashes in 2023, and that safety backdrop has made standard carriers increasingly selective about who they'll cover.

This guide explains what hard-to-place trucking insurance actually is, what triggers the classification, what coverage you need, and how to get it placed — so you can stop chasing dead ends.

Key Takeaways

- Hard-to-place trucking insurance covers fleets that standard carriers decline — due to loss history, new venture status, or high-risk cargo

- E&S (Excess and Surplus lines) markets are built for these risks, with broader underwriting flexibility than standard carriers

- Premiums run higher than standard policies, but specific factors drive cost — and some can be managed

- A broker who specializes in complex trucking risks gets you covered faster — and with fewer gaps

What Is Hard-to-Place Trucking Insurance?

Hard-to-place trucking insurance is coverage for operations that standard carriers won't write — typically because the risk profile falls outside what admitted markets are willing to underwrite at their filed rates.

The Admitted vs. E&S Market Distinction

The difference lies in market structure:

- Admitted carriers follow state-regulated rates and policy forms — they're approved by each state's insurance department and backed by state guaranty funds

- E&S (Excess and Surplus lines) carriers operate with more flexibility. They can cover unusual, high-risk, or unique risks that admitted markets won't touch, and they price those risks accordingly. According to the WSIA, E&S insurers step in when admitted carriers are unwilling or unable to write a risk — and these policies are generally not backed by state guaranty funds

That shift to E&S markets is happening at scale. The U.S. surplus lines market hit nearly $130 billion in direct premiums written in 2024, and commercial auto liability E&S premiums grew 29.1% year over year in the first half of 2025 — a direct signal of how many trucking risks are leaving the standard market.

Who Gets Classified as Hard to Place?

The most common trucking operations that land in non-standard territory:

- For-hire long-haul and interstate carriers

- Hazardous materials haulers (chemicals, flammables, explosives)

- Fuel and petroleum tankers

- Propane/LPG carriers

- Tow trucks and dump trucks

- Car carriers

- New ventures with less than two years of operating history

- Operators with recent at-fault accidents, DUIs, or multiple moving violations

Being hard to place isn't a permanent label. It reflects your current risk profile, and as your safety record, experience, and operations improve, your placement options can shift with them.

Why Truckers Get Classified as Hard to Place

Driving and Safety Record Issues

Underwriters don't just look at the owner's record. Every listed driver gets reviewed, and one high-risk driver in a fleet can affect the entire policy's placement.

At-fault accidents, DUIs, multiple moving violations, and high CSA (Compliance, Safety, Accountability) scores all signal elevated risk. The litigation backdrop makes this worse.

ATRI's research found that trucking verdicts over $1M increased 235% between the 2005–2011 period and 2012–2019, with verdict award size growing 51.7% annually from 2010 to 2018. That exposure has pushed standard carriers to tighten underwriting criteria across the board — meaning operators with any blemish on their record face a much narrower market.

FMCSA's Safety Measurement System (SMS) tracks carriers across seven safety categories including Unsafe Driving, Crash Indicator, and Hours of Service Compliance. High percentile rankings in those categories don't just attract regulatory attention — they're a direct underwriting red flag.

New Ventures and Limited Operating History

A brand-new trucking company has no loss history for underwriters to price against. Without that data, the risk becomes statistically unpredictable, and most admitted carriers won't touch it.

The informal "two-year rule" is real: many markets require at least 1–2 years of operating history before offering standard rates. In practice, that often means new ventures pay double or more what an established carrier pays for comparable coverage.

Cargo Type and Operational Factors

What you haul matters as much as how you drive. High-risk cargo categories push operations out of standard markets:

- Hazardous materials (chemicals, flammables, Division 1.1/1.2/1.3 explosives)

- Petroleum and fuel products

- Propane and LPG

- Oversized or overweight loads

- High-value goods with significant theft or damage exposure

Federal minimum liability requirements reflect this — hazmat haulers transporting certain high-risk materials face a $5,000,000 minimum financial responsibility requirement under 49 CFR Part 387, compared to $750,000 for general freight. Standard carriers often exclude or heavily restrict these cargo classes outright.

Operating radius also factors in. Long-haul interstate routes, cross-border operations, and regions with elevated accident or theft rates all push risk profiles toward non-standard territory.

Coverage Options for Hard-to-Place Trucking Operations

Core Required Coverages

Every trucking operation — standard or hard-to-place — needs these three:

- Primary auto liability — covers bodily injury and property damage to third parties. Required by FMCSA for interstate carriers, with minimums varying by cargo type

- Motor truck cargo — protects the freight being hauled against loss or damage

- Physical damage — collision and comprehensive coverage for the truck itself

For interstate carriers, FMCSA also requires specific filings to remain in legal operation:

- BMC-91: Proof of liability insurance on file with FMCSA

- BMC-34: Required for hazmat carriers as proof of environmental liability coverage

These filings must stay active. A lapse means losing operating authority.

Specialized Coverages for Hard-to-Place Operations

Standard trucking policies leave gaps — especially for owner-operators and non-standard risks. Four coverages that often get missed:

| Coverage | Who Needs It | What It Covers |

|---|---|---|

| Bobtail / Non-Trucking Liability | Owner-operators leased to motor carriers | Truck operating without a trailer or outside of dispatch — the motor carrier's policy won't cover this |

| Trailer Interchange | Drivers using trailers under a written agreement | Physical damage to the non-owned trailer while in your possession |

| Non-Owned Trailer Coverage | Drivers using trailers without a formal agreement | Same protection as trailer interchange — but applies when no interchange agreement exists |

| Occupational Accident | Owner-operators who don't qualify for workers' comp | Wage replacement and medical benefits after an on-the-job injury |

| General Liability | Any trucker with loading dock or facility exposure | Off-road incidents — loading dock injuries, property damage at a customer's site |

Trailer interchange and non-owned trailer coverage are routinely confused. Using the wrong one leaves you unprotected. A broker familiar with trucking placements will distinguish between them upfront.

Soma places all of these coverage types for hard-to-place trucking operations — new ventures, drivers with violations, specialty commodities, and hazmat haulers. Carrier partners include Chubb, Progressive, Kemper, and Ascend. DOT and FMCSA filings are handled as part of the placement process.

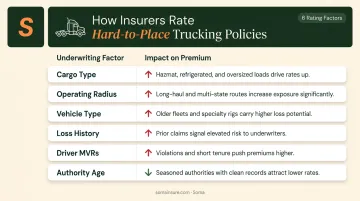

How Insurers Calculate Premiums for High-Risk Truckers

Premium calculations for non-standard trucking risks start with the same factors used in standard markets — then amplified.

Primary rating factors underwriters evaluate:

| Factor | Direction of Impact |

|---|---|

| Cargo type (hazmat, fuel, high-value) | Increases premium significantly |

| Operating radius (local vs. long-haul) | Long-haul raises rates |

| Vehicle type (tanker, dump truck, tractor-trailer) | Specialty equipment = higher cost |

| Loss history | Claims push rates up; clean history reduces them |

| Driver MVRs and CDL experience | Violations and gaps increase premiums |

| Authority age (new venture vs. established) | Newer operations pay more |

The broader market environment pushes hard-to-place premiums higher still. ATRI reported in 2025 that trucking auto liability premiums rose 36% per mile over the past eight years, driven by persistent insurer unprofitability. Liability insurance costs reached 10.2 cents per mile in 2024, up 18.6% from 2021.

Reduced competition compounds the problem. As carriers exit the trucking market, fewer options remain for high-risk operators, which pushes prices up further.

One way to reduce premium outlay: **higher deductibles on physical damage and cargo policies**. A larger deductible shifts more first-dollar risk to the operator in exchange for lower premiums, but it requires adequate cash reserves to cover claims. This option doesn't apply to liability coverage, which is regulated and can't be structured this way.

How to Find and Secure Hard-to-Place Trucking Insurance

Work With a Specialized Broker

A generalist agent or direct carrier channel won't cut it for hard-to-place trucking risks. Standard agents typically have access to a handful of admitted carriers — not the E&S and surplus lines markets where these risks actually get placed.

Shopping multiple agents simultaneously can backfire — and many operators don't realize this until it's too late. In many E&S markets, the first broker to submit an application effectively "blocks" that market from accepting submissions from other agents on the same risk. Spreading your search too widely too fast can close doors.

A specialized commercial trucking broker brings:

- Direct access to E&S and surplus lines carriers

- Multiple carrier relationships across both admitted and non-admitted markets

- Experience structuring submissions that present risk favorably to underwriters

- Knowledge of which carriers have appetite for specific operation types

What to Prepare Before You Approach a Broker

Coming to the table organized significantly improves your chances and speeds up the process. Pull together:

- Loss run history — 3 to 5 years, from all prior carriers

- MVRs for all drivers — current, not older than 30 days

- Business plan and revenue projections — especially critical for new ventures

- DOT number and operating authority documentation

- Safety program documentation — ELD logs, dash cam systems, telematics data, driver training records

That last category matters more than many operators realize. According to FMCSA research, ELDs prevent roughly 1,844 crashes annually. Underwriters know this data — carriers who can show a documented safety culture are seen as meaningfully lower-risk accounts.

Soma works this way by design: gathering the right documentation upfront so submissions reach the right markets quickly, rather than cycling through standard channels where hard-to-place risks often stall for weeks.

Steps to Improve Insurability Over Time

Hard-to-place status isn't permanent. These actions move an operation toward standard market eligibility:

- Maintain a clean loss history for 2–3 consecutive policy years — this is the single biggest factor

- Invest in driver training and document it formally

- Deploy safety technology — telematics, ELDs, and dash cams signal proactive risk management to underwriters

- Keep CSA scores low across all BASIC categories, particularly Unsafe Driving and Crash Indicator

- Build authority tenure — each year of clean operating history narrows the gap between your rates and the standard market

Underwriters notice when renewal submissions include consistent improvement. The goal is giving carriers the concrete data they need to justify moving your risk into a lower-cost tier.

Frequently Asked Questions

What is hard to place insurance?

Hard-to-place insurance covers businesses or operations that standard admitted carriers decline due to elevated risk. These risks are placed instead with specialty or E&S (Excess and Surplus lines) markets, which have the flexibility to underwrite non-standard risks at adjusted rates.

What is the best insurance for a trucking company?

At minimum, every trucking company needs primary auto liability, motor truck cargo, and physical damage coverage. Hard-to-place operators should also carry bobtail, trailer interchange, and occupational accident coverage — a specialized trucking broker can structure the right package for your operation.

What types of trucking operations are hardest to insure?

New ventures under two years old, hazmat and fuel haulers, operators with recent at-fault accidents or DUIs, and specialty vehicle types like tow trucks, dump trucks, and tankers. All of these fall outside the standard underwriting appetite of most admitted carriers.

Can a brand-new trucking company get hard-to-place insurance?

Yes — new ventures can get coverage through E&S or specialty markets, though premiums will run substantially higher than for established operations. A clean driver MVR, CDL experience, a business plan, and documented safety practices all improve placement odds.

How much more expensive is hard-to-place trucking insurance?

Progressive's 2024 data puts national average monthly costs at $746 for specialty truckers and $954 for transport truckers — hard-to-place operations typically pay above those figures. Actual cost depends on cargo type, operating radius, loss history, and authority age, and tends to fall as a clean record accumulates.

How long does it take to move from hard-to-place to standard trucking insurance?

Most underwriters want 2–3 consecutive years of clean loss history, strong CSA scores, and improved driver records before moving a risk to standard market placement. Consistent safety investment and documented improvement can shorten that window.